Talking Points:

- EUR/USD eases as European equities, peripheral credit surge.

- Environment ripe for further Canadian Dollar gains.

- As FX market volatility stays elevated, it's a good time to review risk management principles.

Markets may have been upset with some of the language used by ECB President Mario Draghi in his press conference, but one thing is clear: the ECB delivered. Going into the report, we were looking for a 10-bps rate cut to the deposit rate cut at a minimum, with a small extension to the QE program, and were looking at a coin-flip for whether or not the ECB would expand the run-rate of the program by €10 billion per month.

The ECB did all that and more. All three main rates were cut (deposit, marginal lending facility, and benchmark), the program was extended further, the run-rate was increased by €20 billion per month (to €80 billion per month overall), collateral eligible under the purchase program was expanded to included non-bank corporate bonds, and new TLTROs were unveiled. There is a strong argument to be made that the ECB just fired its bazooka.

The one caveat to everything good about yesterday was that ECB President Draghi suggested that the ECB wasn’t inclined to cut rates further. Markets certainly toiled with this yesterday, as the German DAX dropped around -5% from its highs. His comment, coupled with ongoing commentary from the ECB that the FX channel has weakened - that's to say that a weaker Euro will be harder to come by, and the gains derived from a weaker Euro will limited - made it seem like forward guidance was shutting the door, essentially negating the current set of measures.

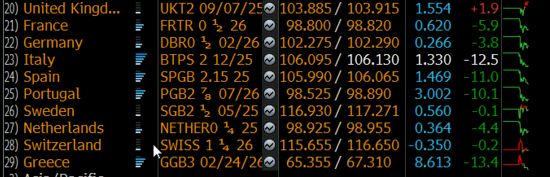

That may be the wrong view.According to the Bank of Spain (per the Wall Street Journal), there are four Euro-Zone countries are on the wrong side of the net-borrowing/lending equation vis-à-vis the European Central Bank and National Central Banks: Italy, Spain, Greece, and Portugal. The day after the ECB's bazooka, here's what European 10-year bonds are doing (table 1 below).

Table 1: European 10-year Bond Yields (Daily Change - March 11, 2016)

Yields are falling across the aforementioned four countries more than anywhere else, and in turn, equity markets across the globe are rallying. The question for investors going forward is whether or not the ECB's measures will be sufficient enough to reduce credit risk. By reducing corporate credit risk (by targeting non-bank corporate debt) and greasing credit channels particularly in the periphery, the ECB is trying to stoke higher lending and borrowing. Reducing risk premia should in turn help buoy asset prices.

Where this impacts the Euro, and how the Euro could be hurt by this, is through the portfolio rebalancing channel. This effect, something that we've seen impact asset prices on and off over the past few years (thanks to QE), dictates that in a falling yield environment (rates in Europe are going further negative - check), investors will be forced to take on greater risk to achieve similar levels of return. If investors outside of the Euro-Zone want to take advantage of falling credit risk and higher equity markets in Europe, they have to exchange their local currencies for Euros.

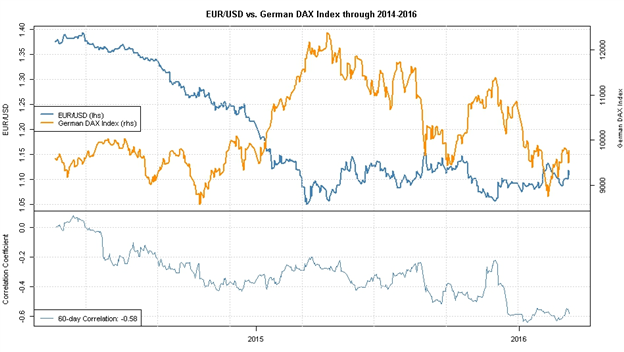

Chart 1: EUR/USD versus German DAX (January 2014 to March 2016)

Currently, the 60-day correlation between EUR/USD and the German DAX is -0.58. This is where the Euro could be impacted: as investors take on EUR-denominated assets onto their balance sheet/into the portfolio, they will need to short the Euro in the spot of forward market in order to limit exchange rate risk. In this case, higher equities - a stronger German DAX, for example - would be bad for the Euro.

See the video (above) for technical considerations in EUR/USD, EUR/GBP, EUR/CAD,USD/CAD, CAD/JPY, Crude Oil (USOIL), and the USDOLLAR Index.

Read more: CAD Enjoying the Ride as Potential for a Bottom in Crude Oil Develops

--- Written by Christopher Vecchio, Currency Strategist

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

To be added to Christopher's e-mail distribution list, please fill out this form